Sunday, November 27, 2016

Background Part 2, The Role of Securitization

The securitization of subprime mortgages into mortgage-backed securities (MBS) and collateralized debt obligations (CDOs) was a major contributing factor in the subprime mortgage crisis. Subprime MBS and CDOs were attractive to investors due to the higher interest rates they offered versus assets backed by prime mortgages. Subprime borrowers with less than perfect credit had higher interest rates on their mortgages due to the increased risk of default. Further, many loans with adjustable-rate mortgages were made that later added a great deal of fuel to the mortgage crisis.

During this time, lenders pooled the subprime mortgages into MBS and CDOs. These financial products often received high ratings from credit agencies. Tranches of these securities were then sold to unsuspecting investors, who were not aware of the risk associated with them. The lower-quality tranches offered higher interest rates but absorbed the first losses associated with defaulting mortgages before the senior tranches.

Subprime lending caused a dramatic increase in available mortgage credit. Many loans were made to borrowers who would have previously had difficulty obtaining mortgages due to below-average credit scores. Private lenders made a lot of money by pooling and selling the subprime mortgages. However, the risk of foreclosure increased with the relaxing of credit standards. Lenders and buyers incorrectly assumed that real estate values were impervious to a downturn. Private-label MBS provided a lot of the necessary capital for the subprime mortgages. Around 80% of subprime loans were made with private-label MBS in 2006. In March 2007, the value of subprime mortgages was valued at around $1.3 trillion. The mortgages issued by private lenders had greater risk since they were not backed by the government, like those from Freddie Mac and Fannie Mae.

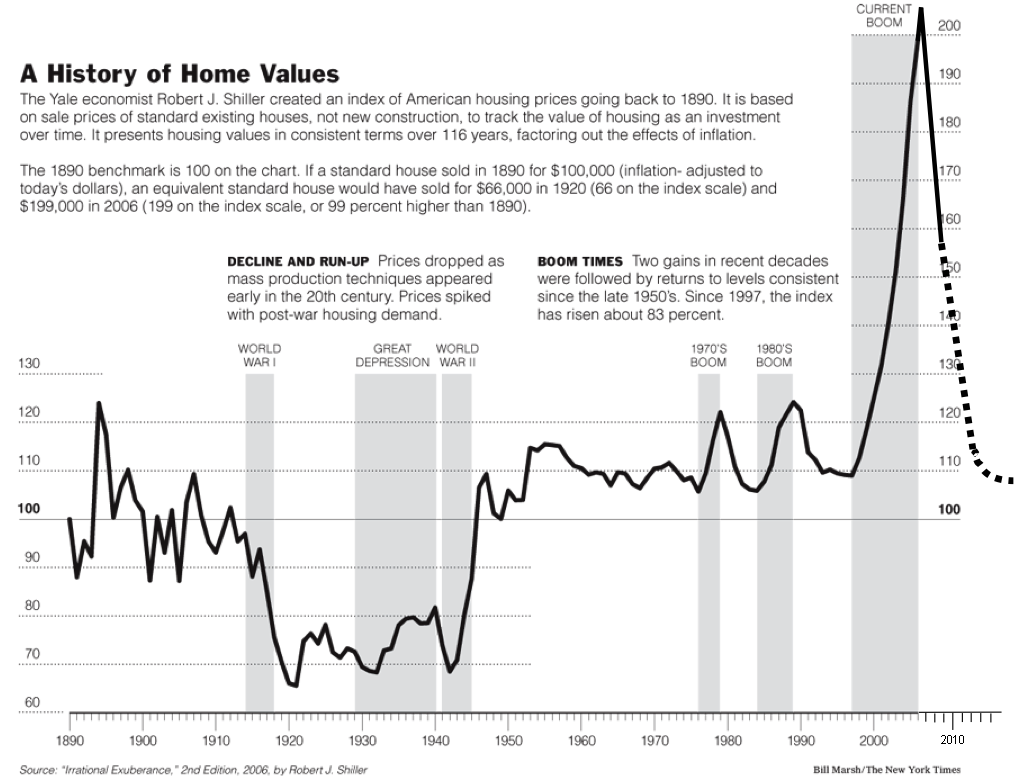

The real estate market boomed, with more buyers bidding up the prices of available houses. The real estate markets in Florida, Arizona and the Las Vegas area were very hot during this time. At first, subprime borrowers who fell behind could refinance their mortgages based on higher property values or could sell homes at a profit. The amount of risk for subprime mortgages was not an issue at this time.

Only when property values began to decline did issues begin to appear. Adjustable-rate mortgages began to reset at higher rates, and mortgage delinquencies grew substantially. The default on subprime mortgages led to more problems. By August 2008, around 9% of all mortgages in the U.S. were in default. MBS and CDOs began to lose value with the higher default rates. Freddie Mac and Fannie Mae were seized by the government in 2008 as they began to realize large losses. Foreclosures and repossessions increased, with more properties being placed on the market as banks attempted to liquidate their inventories. This depressed property values even more, leading to a downward spiral for the real estate market. Some borrowers attempted short sales for their underwater mortgages, but they often found lenders difficult to work with or unwilling to negotiate.

Source: Investopedia http://www.investopedia.com/ask/answers/041515/what-role-did-securitization-play-us-subprime-mortgage-crisis.asp#ixzz4RG8wdyO5

{kind=link}